“How much insurance you should purchase depends on your needs and your lifestyle,” says Dustyn Shroff, Vice President of GreatFlorida Insurance.

In Florida, minimum coverage requirements are $10,000 for personal injury protection (PIP) and $10,000 in property damage liability. This is the lowest level of protection and drivers will pay the least. However, it is usually inadequate if you are involved in an accident.

PIP covers medical expenses due to a car accident, covering the policy holder and passengers regardless who is at fault. It also pays for lost wages and funeral expenses.

Property damage liability covers expenses related to you or someone driving your insured vehicle caused to another person’s property. This includes hitting your neighbor’s mailbox or rear-ending a car at a light. If you are found legally responsible for an accident, any damages costing over $10,000 are your responsibility and you have to pay the difference out of your pocket.

If you want better coverage, you’re going to need to buy more than the minimum requirements. Most experts recommend 100/300/100. That is $100,000 per person for bodily injury liability, $300,000 per accident in bodily injury liability and $100,000 in property damage.

Additional car insurance you will want to consider includes, collision and comprehensive to cover accidents, repairs, theft, vandalism and flooding among other incidents. It will cover the current market value and replacement costs of your vehicle and might be required if you have a car loan. In Florida, comprehensive car insurance also pays for free windshield repair.

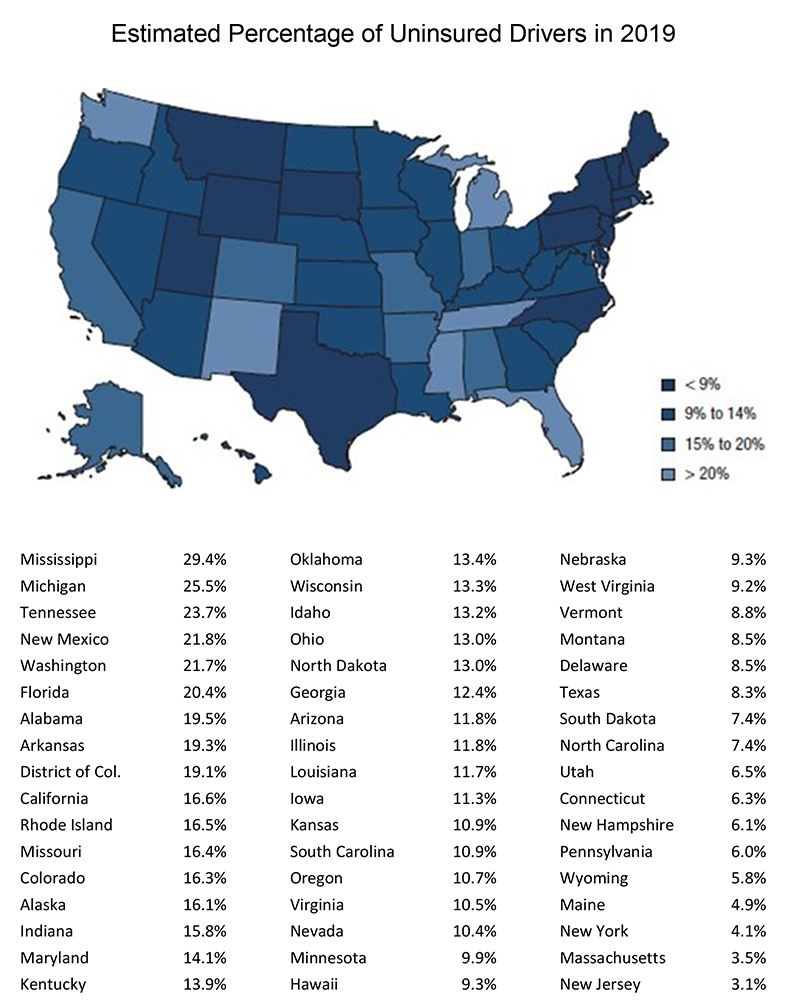

A popular car insurance option includes insurance against uninsured or underinsured motorists. The Insurance Research Council reports there are 20.4% uninsured motorist driving cars in Florida, one of the highest rates in the country.

There are several coverage types to choose from. With a basic knowledge of the main types of car insurance, you can put together a good policy that fits your specific insurance needs.

Additional car insurance includes:

- Roadside assistance – pays for a locksmith or tow truck

- Rental reimbursement – pays for a rental car or other transportation while your car is being repaired

- Gap insurance – covers the cost between the actual cash value and how much is owed on your car loan.

- Custom equipment coverage – reimburses for the expense of custom or aftermarket parts that are damaged in a collision.

For extra liability insurance above your base auto policy, look into getting an umbrella insurance policy. For a relatively inexpensive amount you can buy an extra $1 million or more in liability coverage through an umbrella policy.

“In Florida, insurance follows the vehicle, not the driver,” says Dustyn Shroff, Vice President of GreatFlorida Insurance. This means your coverage still applies even if someone else is driving your car during an accident.

Part of the auto insurance buying process requires the driver to decide on a deductible. This is the amount you pay on a claim before the insurance company reimburses you. The higher the deductible, the lower the premium.

A number of factors are evaluated to determine the cost of auto insurance including, the insured’s age, zip code, driving history and credit score. Auto insurance companies calculate their rates differently. Be sure to ask your agent about discounts, plenty are available.

When selecting insurance, service as well as affordability should be a consideration. If you get into a car accident, you want to be sure your insurance company will make the insurance claims process goes as smoothly as possible.

Are you looking for car insurance? Contact GreatFlorida Insurance agents who will seek out the best policy to suit your needs and fit your budget.